The construction industry stands at a pivotal moment. While headlines focus on artificial intelligence disrupting white-collar work, AI is simultaneously driving one of the largest construction booms in modern history—and fundamentally changing how buildings get built.

The AI Infrastructure Surge

Data center construction has reached unprecedented levels. Primary market supply hit approximately 8,155 megawatts in the first half of 2025, with vacancy rates hovering around a remarkably tight 1.6%. The pipeline stands at roughly 8 gigawatts, and most of that capacity is already pre-leased. Industry forecasts expect vacancy to remain below 5% through 2027, ensuring construction activity will continue at this elevated pace.

The numbers tell a compelling story: annualized data center construction spending reached approximately $40 billion in June 2025, representing a 30% year-over-year increase following an already robust 2024. The catalyst is clear—surging demand for AI computing capacity is driving an infrastructure build-out on a scale rarely seen outside wartime mobilization.

A Labor Market Running Hot

Despite cyclical cooling in portions of the residential sector during 2025, construction labor markets remain exceptionally tight. The Associated Builders and Contractors estimates the industry must attract roughly 439,000 net new workers in 2025, with that figure rising to approximately 499,000 in 2026 to meet demand. Job opening rates climbed to 3.5% in July 2025, and wage pressure continues to run elevated across most trades.

This persistent tightness creates both challenges and opportunities. Contractors struggle to staff projects on schedule, while workers with in-demand skills command premium compensation. The question on every industry leader’s mind: will technology ease these constraints or accelerate them?

How Technology is Transforming the Work

The same AI revolution driving data center demand is beginning to reshape construction execution itself, though adoption remains uneven across the industry.

Planning and Coordination

Generative AI and machine learning tools are optimizing schedules, logistics, and clash detection with unprecedented sophistication. The result: fewer coordinators can manage larger project scopes, raising output per project manager and engineer. What once required multiple specialists reviewing drawings can now be augmented by algorithms that flag conflicts before they reach the field.

Field Execution

Task-specific robotics are moving from pilot programs to real deployments. Layout printing robots, automated rebar tying systems, precision drilling equipment, drywall finishing machines, and autonomous excavation units are reducing crew sizes on repetitive, precision-driven tasks. Skilled operators and technicians are replacing portions of traditional general labor roles.

Academic and industry studies report productivity gains of up to 35% on targeted workflows where these technologies are deployed—though these improvements aren’t yet generalizable to entire projects. The technology excels at repetitive, measurable tasks in controlled conditions but still struggles with the variability and problem-solving that characterizes much of construction work.

Quality Assurance and Reality Capture

Drones and computer vision systems are shifting superintendent and quality assurance workflows. Rather than spending hours walking sites and marking up issues, these professionals increasingly focus on exception handling, reviewing digital models that flag deviations automatically.

The Adoption Reality

Interest in construction technology runs high, but 2025 reports show pilot programs significantly outpacing scaled rollouts. Implementation remains uneven, concentrated in larger firms and specific project types. Nevertheless, market analysts forecast sustained double-digit growth for construction robotics—approximately 14-18% compound annual growth rates into the 2030s—albeit from a relatively small base.

The Net Effect: Displacement Without Mass Unemployment

The employment picture emerging from this technological shift defies simple narratives of either job destruction or unbounded growth.

Robots and AI are removing specific person-hours per task—a surgical displacement rather than a sweeping one. Simultaneously, total work volume driven by AI infrastructure, data center builds, and sustained public and industrial spending keeps overall labor demand elevated. The result is a skill mix shifting upward while total headcount pressure persists.

Workers aren’t being replaced wholesale; rather, the nature of construction work is evolving toward higher-skilled, technology-enabled roles.

The Five to Ten Year Outlook

Base Case Scenario (Most Likely)

Through 2026-2030, data center construction, industrial projects, and grid infrastructure upgrades will sustain above-trend nonresidential demand, while residential construction follows its typical cyclical pattern. Labor markets will remain tight but less extreme than the 2021-2023 period.

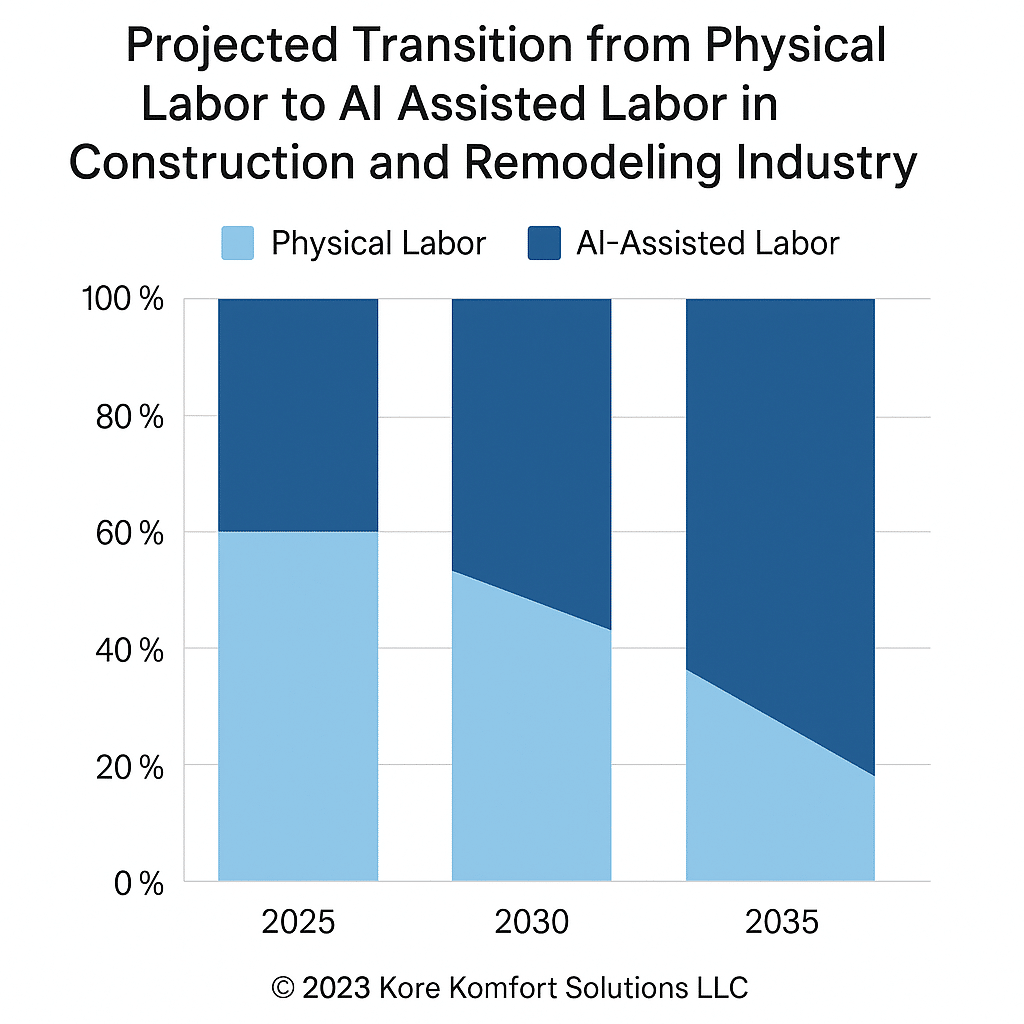

AI and robotics adoption will scale in specific “islands”—layout work, drilling operations, mechanical tie-ins, and finishing tasks—trimming 5-15% of task hours where deployed. Net sector employment will edge upward or hold steady compared to today’s levels, but with significantly higher productivity per worker and premium compensation for tech-literate tradespeople and foremen.

The skills commanding premium wages will include: BIM and Virtual Design & Construction expertise, reality-capture operations, robot operation and maintenance, low-voltage and controls work, commissioning capabilities, and safety and compliance knowledge for high-energy sites involving high-voltage and medium-voltage systems, battery installations, and liquid cooling infrastructure.

Upside Scenario (Accelerated Automation)

If hyperscaler AI capital expenditures remain elevated and equipment vendors successfully develop ruggedized, multi-task robots, labor productivity gains could broaden to 15-25% on repetitive scopes by 2030. In this scenario, labor shortages ease without mass layoffs; headcount growth slows as output per worker rises substantially.

Downside Scenario (Infrastructure Bottlenecks)

If grid interconnection delays and local community resistance defer project starts, and residential softness persists, the picture changes. If robotics deployments plateau at pilot scale, productivity gains remain narrow and concentrated. Under these conditions, hiring needs would fall back toward replacement levels but likely remain positive in data center construction clusters.

Data Center Construction: A Labor Market Within a Market

Data center projects create persistent demand for specific trades: MEP (mechanical, electrical, and plumbing), civil and site work, building envelope specialists, fire and life safety technicians, controls experts, and commissioning professionals. This demand concentrates in specific geographic clusters—Northern Virginia, Phoenix, Dallas, Columbus, and Kansas City lead the list.

The high percentage of pre-leasing and sub-2% vacancy rates provide unusual pipeline visibility for the construction industry, signaling multi-year staffing continuity rather than the boom-bust cycles that plague other sectors.

AI infrastructure raises project complexity significantly. There’s more low-voltage work, more fiber installation, more liquid cooling systems, and more critical-power infrastructure. This translates to a higher ratio of testing and commissioning technicians relative to general labor. While productivity tools compress overall schedules, peak-staffing events still occur and still require substantial crews.

The Bottom Line for Construction Professionals

The next five to ten years will not bring broad job collapse in construction. Instead, expect a steady shift from pure manual labor toward tech-enabled trades. AI and robotics will eliminate pockets of manual work hours, but the AI infrastructure build-out will backfill that demand with new, often more complex work.

Wage pressure and job vacancies will moderate from recent extremes but persist in regions where data center pipelines, power infrastructure projects, and industrial reshoring initiatives converge.

For construction firms, the imperative is clear: invest in workforce development that emphasizes technology literacy alongside traditional craft skills. For workers, the message is equally direct: roles combining hands-on expertise with digital tools and systems thinking will command the strongest demand and highest compensation.

The construction industry isn’t being automated away—it’s being elevated. The future belongs to those who can bridge the worlds of traditional craft and emerging technology.

Kore Komfort Solutions partners with construction firms navigating this evolving landscape, providing workforce solutions that match the right skills to tomorrow’s building challenges.